£880 annual increase in tracker mortgage costs following latest base rate rise

Since December last year, the average monthly tracker mortgage payment has increased by around £3,410 per year, according to UK Finance figures.

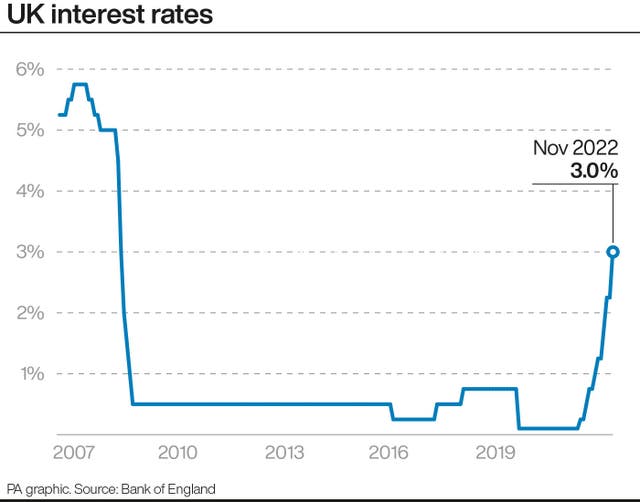

People with a mortgage which directly tracks the Bank of England base rate will see their monthly payments rise by another £73 typically as a result of Thursday’s rate hike.

It is the latest in a string of base rate increases, meaning that, since December last year, the average monthly tracker mortgage payment will have increased by £284.17 in total, according to figures from trade association UK Finance.

This adds up to an increase of around £3,410 per year typically that tracker mortgage holders need to find in their budgets.

The base rate increase from 2.25% to 3% on Thursday will mean a £73.49 monthly increase – or around an extra £880 per year – for the average tracker mortgage holder.

Just under one in 10 (9%) outstanding residential mortgages are trackers and around four in five (78%) are fixed-rate deals.

Chancellor Jeremy Hunt said: “Today’s news is going to be very tough for families with mortgages up and down the country, for businesses with loans.

“But there is a global economic crisis, the International Monetary Fund say a third of the world’s economy is now in recession.”

The average standard variable rate (SVR) mortgage meanwhile will increase by £46.22 per month, according to UK Finance’s figures, if a borrower’s lender passes on the base rate increase in full.

SVRs are set individually by lenders and borrowers often end up sitting on them when their initial deal comes to an end.

The average monthly SVR cost for a borrower has increased by £178.70 in total since December, assuming that base rate increases are being passed on in full.

Bank of England figures released earlier this week revealed that mortgage approvals for house purchases decreased significantly to 66,800 in September, from 74,400 in August.

Base rate rises are not the only factor used by lenders to price their mortgages.

Market volatility following the mini-budget prompted a surge in the mortgage rates being offered by lenders, with many products being pulled from sale.

A recent Office for National Statistics (ONS) survey found that 48% of mortgage holders reported being worried about changes in interest rates on their mortgage.

Stretched mortgage affordability will also have an impact on the housing market.

Savills released a forecast on Thursday suggesting that average house prices across Britain could fall by 10% next year, before starting to climb back upwards from 2024 as expected interest rates and affordability pressures ease.

While fixed-rate mortgage holders are cushioned from the immediate impacts of the base rate rise, many may end up getting a payment shock when they eventually come off their deal, with around 1.8 million fixed deals scheduled to end next year.

In a press conference following the rates decision, Bank of England Governor Andrew Bailey said: “We do understand the difficulties of the situation we’re in and the difficulties mortgage holders face.”

He added that the market expects mortgage rates to drop.

Simon Rubinsohn, chief economist at the Royal Institution of Chartered Surveyors (Rics) said: “Although parts of the economy are still showing some resilience in the face of rising interest rates, the impact of these rises are clearly now being felt in much of the property and construction sectors.

“Today’s move, which is unlikely to be the last, will encourage greater caution both amongst both potential buyers and developers, casting further doubt on the probability of the Government meeting its restated target of building 300,000 homes a year by the mid-2020s.

“That said, preventing inflation expectations getting out of hand is critical. The failure to do so would be more damaging for the economy, households and businesses.”

Jason Tebb, chief executive officer of property search website OnTheMarket.com said: “This latest interest rate rise will only spur on those buyers who managed to obtain a mortgage offer before fixed-rate mortgage pricing shot up following the mini-budget. These comparatively cheap rates will focus buyers’ minds, with many keen to proceed with a property purchase before they elapse.”

Richard Donnell, executive director of research at Zoopla said: “Home buyers need to realise that 4% to 5% mortgages are set to be the norm in future, not the 1% to 2% of recent years.”

Alex Maddox, capital markets and digital director at Kensington Mortgages said: “Today’s result will hit hard for households, homeowners and prospective buyers.”

Sarah Thompson, managing director of Mortgage Scout, said: “Consulting a mortgage broker would be a good idea if you are ready to commit to a home, as they can help you find the deal that is best for you.”

Tomer Aboody, director of property lender MT Finance, said: “Rising inflation, coupled with the disastrous mini-budget, mean this rate rise was always on the cards. Borrowers need to come to terms with the new norm, which is higher interest rates – the rock-bottom rates of the past are long gone.”

Brian Murphy, head of lending at the Mortgage Advice Bureau said: “Expectations are that the industry will see an upwards trend of defaults on mortgage payments in the coming months, and so we urge anyone fearing that they may struggle with mortgage payments to go straight to their mortgage provider for guidance.”