Average UK house price falls by £4,000 month-on-month, report shows

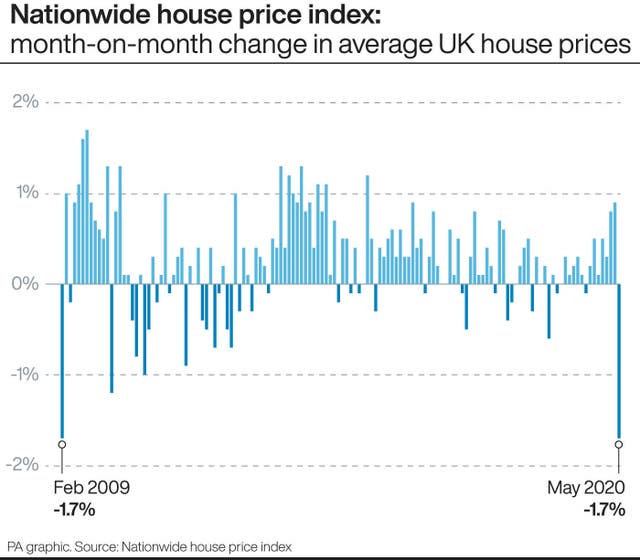

Nationwide Building Society said it was the largest monthly fall since February 2009.

More than £4,000 was wiped off the average house price in May, marking the biggest monthly fall in property values in 11 years, according to an index.

The fall, described as a “car crash” by one estate agent, came after property values had previously hit a record high in April.

Across the UK, property values fell by 1.7% month-on-month in May, the report from Nationwide Building Society said.

It was the biggest month-on-month fall since February 2009 and pushed the average house price in May down to £218,902.

In April, the average UK house price was £4,013 higher, at £222,915. April’s house price index was a record high in cash terms.

Robert Gardner, Nationwide’s chief economist, said: “UK house prices fell by 1.7% over the month in May, after taking account of seasonal effects – this is the largest monthly fall since February 2009.

“As a result, the annual rate of house price growth slowed to 1.8%, from 3.7% in April.

“In the opening months of 2020, before the pandemic struck the UK, the housing market had been steadily gathering momentum.

“Activity levels and price growth were edging up thanks to continued robust labour market conditions, low borrowing costs and a more stable political backdrop following the general election.

“But housing market activity has slowed sharply as a result of the measures implemented to control the spread of (coronavirus).

“Indeed, data from HMRC showed that residential property transactions were down 53% in April compared with the same month in 2019.”

Mr Gardner said the medium-term outlook for the housing market remains highly uncertain and much will depend on the performance of the wider economy.

He said: “The raft of policies adopted to support the economy, including to protect businesses and jobs, to support people’s incomes and keep borrowing costs down, should set the stage for a rebound once the shock passes, and help limit long-term damage to the economy.

“These same measures should also help ensure the impact on the housing market will ultimately be less than would normally be associated with an economic shock of this magnitude.”

Jeremy Leaf, a north London estate agent and a former residential chairman of the Royal Institution of Chartered Surveyors, said: “The extent of the car crash that hit the property market in May is laid bare in Nationwide’s report of the largest monthly fall in house prices for over 11 years.”

He continued: “Uncertainty remains as to the direction of travel for values in some price ranges and locations until momentum begins to build again. The market feels a bit like returning after the Christmas/new year break, with buyers and sellers waiting to see who will blink first as prices establish their post-Covid level.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “As physical valuations return, lenders are able to offer higher loan-to-values once more, returning to larger loans on the high street and in some instances interest-only borrowing.

“With some lenders cutting mortgage rates to ever lower levels, they are sending out a clear message to borrowers that they are open for business.”

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said: “The big month-to-month drop in Nationwide’s house price index in May – the largest since February 2009 – surely is just the start of a protracted decline over the remainder of this year.”

He added: “Unless a full V-shaped recovery emerges in the next six months, the unemployment rate likely will exceed its peak of 8.5% in the wake of the last recession.

“Admittedly, banks are in a much better position than 12 years ago to lend, given their high capital ratios and their ability to access cheap funds from the Bank of England’s latest Term Funding Scheme.”

Mr Tombs said: “Relatively few people likely will be forced to sell their homes, given that mortgage payment holidays are easily available and home ownership has declined.

“Nonetheless, the huge size of the blow from Covid-19 to households’ incomes and the deterioration in consumers’ confidence suggests that house prices must drop.”